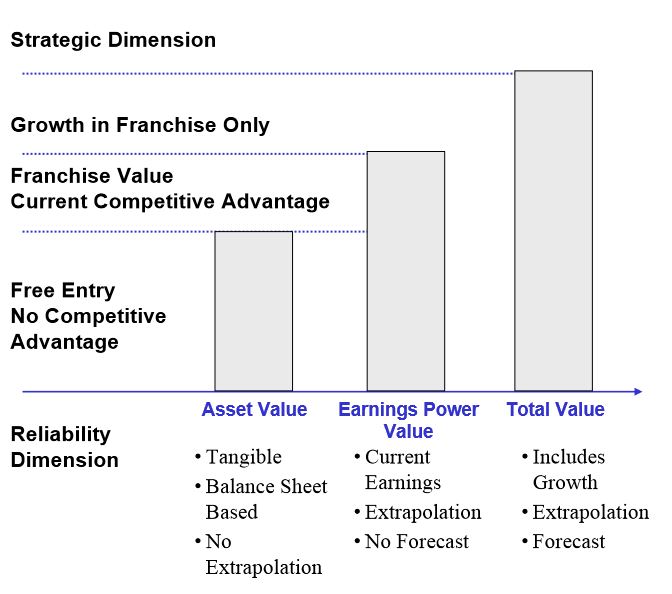

What is franchise value ?

For some reason, there’s always mystique in the air whenever franchise value is discussed. Everybody wants it but few find it, especially in time.

So how can franchise value be identified with accuracy? And more importantly, why does everyone want it so badly?

Luckily for us, wise value investors have not only identified franchise value, but laid out the road map to identify it successfully.

Franchise Value becomes clearer with the help of Warren Buffett and Bruce Greenwald.

Buffett and Greenwald Happily Together Again

Warren Buffett’s Perspective on Franchise Value

Listen to what Buffett has to say about franchise value.

“If you got the right kind of product, you may be paying for taste, you may be paying for a mental association that you have, or service availability. That’s franchise value, then the question is how durable and big is it? I’d say that franchise is basically like a moat around your economic castle.” – Warren Buffett

In Berkshire’s 1991 letter to shareholders, Buffett laid it out in his straight-forward manner.

There are 2 kinds of enterprises

- a business

- and a franchise

He argues that most operations fall in some middle ground, in the sense that they are either a weak franchise or strong business.

He also mentions that an economic franchise arises from a product or service that contains the following characteristics:

- It is needed or desired

- Thought by its customers to have no close substitute

- Not subject to price regulation

A franchise can price its products aggressively and still earn high rates of return on capital. More importantly, franchises can tolerate mis-management.

Buffett said the same thing.

I try to buy stock in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.

Bruce Greenwald’s Perspective on Franchise Value

If you don’t know Bruce Greenwald, he is currently the value investing professor at Columbia University. He also wrote Value Investing: From Graham to Buffett and Beyond which dives into the topic of franchise value.

Literally, Bruce Greenwald is a master when it comes to the topic of franchise value. Best of all, he developed a quantifiable way of measuring franchise value.

But before going into that (here is Jae’s article going over the numbers) I’ll touch on what Mr. Greenwald considers a franchise.

How to Determine Whether a Business is Considered a Franchise

A franchise only exists where a firm benefits from barriers to entry that keep out potential competitors or insure that if they choose to enter, they will operate at a competitive disadvantage relative to the incumbents. These need to be identifiable and structural.

Good management is certainly an advantage, but there is nothing built in to the competitive situation to guarantee that one company’s superiority on the talent count will endure over time. Structural competitive advantages come in only a few forms:

- Exclusive governmental licenses

- Consumer (demand) preferences

- A cost (supply) position based on long-lived patents or durable superiorities

- Combination of economies of scale thanks to a leading share in the relevant market with consumer preference

Bringing the Franchise Value Concept Together

All of Buffett’s and Greenwald’s points interconnect. Durable competitive advantages have nothing to do with size, trends, patents or outstanding sales numbers by themselves.

Think about this.

What is the use of having an extremely efficient and large corporation if there’s no sustainable demand for its products?

The characteristics of a franchise act as links. If you look at the image below, each circle on its own is not important. Only when they are connected and feeding each other does it really strengthen up.

If one of the links weaken, the whole franchise starts to erode and eventually the competition will catch up.

The Franchise Circle of Life

Coca Cola’s Franchise Value

Coca-Cola is a company that has all of these characteristics. And there’s a reason why Buffett purchased like crazy in 1988.

Charlie Munger dedicated some of his talks to discuss what makes Coca-Cola tick. So let’s grab some of his ideas and apply them into each of the franchise’s links.

1) Pricing Power – Do you think people will pay a few extra cents to get their hands on a bottle of Coke? AskDavide Andreani.

Davide Andreani’s Lifelong Dedication to Coca Cola

2) External Protection – Coca-Cola’s business is simple. They sell syrup and licenses to produce a beverage containing the syrup.

How is it possible that more than a century later, Coke survived “destructive competition” as Munger puts it?

Coca Cola protects its patents, trademarks and recipes like a mad man. Even if there are similar products, it’s just not a Coke.

3) Customer Demand – Munger narrowed down Coca-Cola’s advantages to a combination of physiological and psychological factors.

- Coke is a cold beverage. It can be taken repeatedly, as opposed to hot beverages.

- Coke’s recipe was developed to disappear immediately from your mouth. Have you every paid attention to this? Try it. Take a sip, 2 seconds later the taste is gone. No wonder people are addicted to Coke. Here’s a lady that drinks 50 cans a day.

- What images come up in your mind when you hear “Coke”? I’m going to guess that it is at least one of the following; summer, happiness, refreshing, friendship, great athletes. (I’ll pass the tipping jar later)

The overall result: a socially accepted and desired beverage that you can drink repeatedly. It’ll take you to a state of temporary freshness and happiness.

(Where’s my Coke already?)

4) Economies of scale - As of 2013, 1.8 billion Coke servings was consumed per-day.

That’s right, per day.

The important thing to identify is that a company that grows so much is benefited by having all the previous franchise value factors operating seamlessly together.

This ensures expansion, marketing, advertising and more importantly, brand protection efforts help to create profit, and not to simply maintain and cover cost.

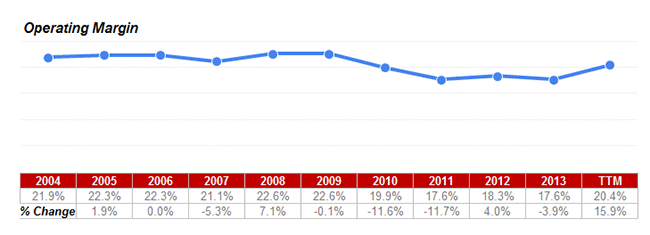

Fundamentals from a Franchise

Earnings and cash flows are easier to predict when franchises are identified.

Take a look at KO’s Operating Margin and EPS.

KO Excellent Operating Margins

Margins have taken a dip from 2010. But it’s in the high teens but latest TTM numbers are showing a strong rebound.

And now check out the growth in earnings and the steady expectations upwards.

Coca Cola EPS and Quick Valuation using the Graham Formula

And here is Coca-Cola’s official statement on dividends.

The Coca-Cola Company has paid a quarterly dividend since 1920 and has increased dividends in each of the last 50 years. The dividend payment amount below is the actual amount paid per common share.

Look at the return cousins (ROE, ROA, ROIC and CROIC). Stability’s the name of the game.

Coca Cola Excellent Returns | Click to Enlarge

Learn more about how to interpret these numbers and what to look for in the financial statements to interpret a competitive advantage. Competitive advantage is a key point in determine whether a franchise exists.

Now combine this fundamental research with your experience and circle of competence.

That’s a triple deadly combo.

Franchise Value is Harder to Find than an Easter Egg

Here’s another quote from Greenwald that you should remember.

Growth creates value only when it takes place within the limits of a strong and sustainable company franchise, and these are rare. Second, not all growth – even growth that is worth something – can be appraised with enough precision to permit an accurate valuation.

Identifying, understanding and valuing franchise value is no easy task. He even goes on to say how rare it is. Many investors mistakenly assume that a brand name company is a franchise, but you need numbers to back it up. In Coca-Cola’s case, you have high double digit returns going back several decades.

Greenwald is a straight up franchise value seeking guy so it’s not uncommon for him to say these things.

…Otherwise, the value investor is just another punter, taking a flier rather than making an investment.

Buffett purchased it in 1988 back when Coca-Cola was a small to mid cap company. He already possessed uncanny business acumen and was able to identify the hidden franchise within the company. For the rest of us, it takes time to develop the skill. Not to mention the discipline and patience to wait for the right pitch to hit it out of the park.

That’s where a lot new investors struggle.

- How are you at identifying franchises?

- What metrics do you use?

- Do you always seek a stock with franchise value?

http://www.oldschoolvalue.com/blog/investing-perspective/franchise-value/